$1B-plus in take-out financing likely for Tishman, Rockrose, in LIC this year

Tishman Speyer and Rockrose are likely to obtain Long Island City take-out loans valued in aggregate at $1 billion or more this year (Photo: Google)

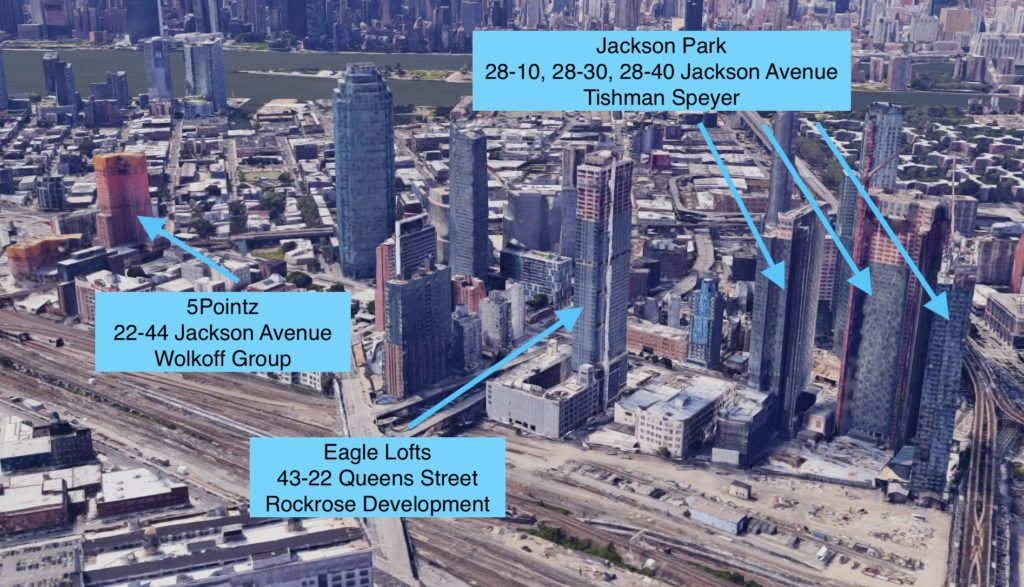

Developers have opened large rental towers in growing Queens market

By Adam Pincus

Tishman Speyer and Rockrose Development are likely the next builders to announce large take-out loans for completed rental towers in Long Island City, with the combined debt almost certain to top $1 billion.

Tishman completed three towers with a total of 1,777 apartments between December 2017 and June 2018. The firm currently has a $640 million construction loan package through Bank of America and Wells Fargo.

Meanwhile Rockrose opened the 790-unit Eagle Lofts at 43-22 Queens Street last year, after obtaining its initial temporary certificate of occupancy in June 2018. The $255 million construction loan, also from Bank of America, was issued in April 2017.

For 12 rental projects greater than 200 units completed in Long Island City since 2012, the average between the initial temporary certificate of occupancy and the take-out loan was 289 days, a review by PincusCo Media found.

The upcoming debt deals will define the market in the post-Amazon world. The real estate market in Long Island City was whipsawed in a brief period, first with the news in November 2018 that Amazon would introduce 25,000 workers into a new campus over the next decade, and then three months later the news they were backing out. There was a reported surge in demand for residential condos, and now that demand has reportedly declined.

Yet the rental market, according to brokers, was largely unaffected and is considered strong. The net rental rate in Long Island City rose by 12 percent over 2018 as of the fourth quarter of last year, to about $3,400 per month, information from brokerage Modern Spaces showed.

“Today, when I am calling lenders and say I have a project in Long Island City, no one says, ‘Hey, Amazon is not coming!’ It continues to be a very strong market,” said Abraham Bergman, managing partner at brokerage Eastern Union Funding.

Even the more than 2,500 rental units added by Tishman and Rockrose have not upended the market, said Eric Benaim, CEO of brokerage Modern Spaces.

“To be honest, at first I was a little worried, but they are absorbing pretty quickly, at a good clip. So that concern is gone,” Benaim said. He estimated about 80 percent of those units had been absorbed.

PincusCo took a look at more than two dozen rental projects with 200 units or more in Long Island City which were recently started or completed, to get a sense of the financing market Tishman and Rockrose will be operating in. Tishman and Rockrose declined to comment for this article.

Most firms start looking for take-out financing as they approach the 90 percent leased stage, in part because Fannie Mae generally requires rental buildings to be 90 percent occupied for 90 days, known informally as the “90 for 90” rule, before they will approve a loan deal.

Although Tishman and Rockrose don’t typically take out bridge loans for recently completed projects, there are developers choosing them, said David Eyzenberg, president of Eyzenberg & Company, a commercial real estate-focused investment bank.

“Some borrowers look to do a bridge loan post construction until they achieve stabilization,” Eyzenberg said in an email.

Of 14 large cash-flowing buildings analyzed, either Fannie Mae or Freddie Mac was involved with eight of them, totaling just over $1 billion in secured debt. The other loans were provided by life companies including MetLife, and Massachusetts Mutual Life; or other lenders such as Morgan Stanley.

While the occupied-building market is dominated by Fannie Mae, the construction lending market in LIC is more diverse. Of the $2.8 billion in deployed in large rental construction financing in LIC, Bank of America has the largest chunk, with $895 million, as the lender on the completed Tishman and Rockrose projects.

Other major lenders include M&T Bank, Bank OZK, Wells Fargo and JPMorgan Chase.

While most developers shoot for take-out loans after the building is 90 percent occupied, there’s less consistency in timing for construction loans. For example the Durst Organization obtained $360 million in financing from M&T Bank in December 2018 for its 958-unit tower Queens Plaza Park at 29-37 41st Avenue, just a month after new building permits were issued.

Others, like Rockrose and the Wolkoff Group, did not take their construction loans until much later in the process, after many stories of the structure had been raised.

For example, the Wolkoff Group is developing the 1,115-unit 5Pointz at 22-44 Jackson Avenue. The firm obtained its new building permit in May 2015, but did not get construction financing — $300 million from Bank of the Ozarks, now Bank OZK — until November 2017, after much of the complex had been built.

Just six months later, in May 2018, Wolkoff filed for an initial temporary certificate of occupancy (TCO), indicating the towers were nearing completion, and that soon tenants can move in. The city has not issued the TCO, however, a review of New York City Department of Buildings records show.

“It was easier for us to just start going to work without any financing. We knew the more we put of our money in, the less risk to the lender,” which allows the firm to obtain relatively better terms and rates, said David Wolkoff of the Wolkoff Group. He said on smaller projects his firm will forgo lenders completely.

Rockrose, at Eagle Lofts, obtained new building permits in May 2015, but did not close on financing until April of 2017, after much of the superstructure was complete. The decision to delay was all about minimizing the costs of funds. The firm began to delay the construction loan because of a change banks made about a decade ago.

At that time, construction lenders began charging developers a non-use fee for money the bank had committed to on a construction loan but had not yet funded. So Rockrose now waits until virtually all the project’s equity is spent on construction before finalizing the loan, a source familiar with their financing said.

That strategy is possible because the firm has a long, successful development track record and strong lender relationships so is not worried about starting a project and not getting funding, the source said.